Collecting funding on dYdX - a bulletproof strategy for yield enjoyers

Happy Saturday, friends!

Inefficiencies exist in the crypto perpetual market, and traders can take advantage of mispricings and earn a profit.

The cash and carry trade is a profitable strategy that allows traders to take advantage of the discrepancies between perpetual and spot price.

Today I wanted to take you through how you can set up a delta-neutral trade on dYdX, and collect funding every hour for doing so.

dYdX is the only decentralized exchange that Ethena uses for its delta-neutral strategy, which is a huge trust stamp IMO.

Collecting funding on dYdX - a bulletproof strategy for yield enjoyers

Inefficiencies exist in the crypto perpetual market, and traders can take advantage of mispricings and earn a profit. The cash and carry trade is a profitable strategy that allows traders to take advantage of the discrepancies between perpetual and spot price.

Today I wanted to take you through how you can set up a delta-neutral trade on dYdX, and collect funding every hour for doing so.

dYdX is the only decentralized exchange that Ethena uses for its delta-neutral strategy, you can verify this here: https://app.ethena.fi/dashboards/hedging/BTC

Traders can utilize both CEX’es and DEX’es to take arbitrage positions without exposing themselves to high fees. You can use this strategy to take long positions in assets while simultaneously selling associated futures derivatives and earn the funding rate when the market is long-skewed. For some of you this may sound very advanced, but rest assured, I will break it down ELI5-style.

What is the funding rate?

The funding rate is a recurring payment that traders pay or receive based on the disparity between perpetual contracts and spot prices. This rate is determined by the skew of the derivative and the extent to which the perpetual contract deviates from the spot market.

When a Perpetual Swap contract trades at a premium, the skew on dYdX/Binance/Bybit/ has turned positive. Similarly, when the Perpetual Swap contract trades at a discount, the skew on the DEX/CEX has turned negative.

Basically what we are going to do is to do what Ethena Labs is doing (long ETH spot, short ETH perp), but we are going to do it ourselves + we are going to choose the asset we want (hint: it doesn’t have to be ETH).

If you’re not sure about what Ethenea Labs is, I wrote about them here:

If you don’t want to read that, I’ll try to explain it as easily as I can.

If we use Bitcoin as an example, we want to go long BTC.

So if we long BTC spot on an exchange or buy WBTC on eg. Uniswap, and we want to short $BTC on perp (eg. on dYdX).

So if we are equally long and short, we will be delta neutral. This means that no matter what happens to the BTC price, we will not lose/earn money by BTC price fluctuation.

A delta-neutral strategy is one that attempts to construct a portfolio or group of positions that have no directional risk to the market. For example, if I both open a long trade of 1 BTC and a short trade of 1 BTC at the exact same price, then regardless of the movement of the market, my total portfolio value will not change (ignoring fees).

What we will earn money from is the funding rate on BTC.

Funding is the primary mechanism to ensure that the last traded price is always anchored to the global spot price. It is similar to the interest cost of holding a position in spot margin trading.

The funding fee is exchanged directly between buyers and sellers at the end of every funding interval. Using an 8-hour funding time interval as an example, funding will occur at 12 AM UTC, 8 AM UTC, and 4 PM UTC.

Note that on DEX’es like dYdX, funding is paid/recieved every 1 hour, not every 8 hour as on Binance/Bybit.

When the funding rate is positive, long position holders pay the short position holders. Likewise, when the funding rate is negative, short position holders pay the long position holders (this is the case for bull markets, I will come back to this)

Traders will only pay or receive a funding fee if they hold a position at the funding interval (12 AM UTC, 8 AM UTC, and 4 PM UTC). Unless you use dYdX or a DEX which is every hour

If positions are entirely closed prior to the funding exchange then traders will not pay or receive funding fees.

The funding fee charged will be deducted from the trader's available balance. In the event where the trader has no sufficient available balance, the funding fee will be deducted from the position margin and the liquidation price of the position will be more prone to the mark price. The risk of liquidation will increase.

To calculate the annual APR using the funding rate above the calculation is as follows:

For dYdX:

0.003636% * 24 = 0.087264% (1 day APR)

0.087264% * 365 = 31,85% (1 year APR)

When the funding rate is positive (as per our example) traders that are long pay the funding rate whereas traders who are short receive the funding rate. This is important as it sets the stage for understanding how we can build delta-neutral strategies to use the funding rate to our advantage.

Your daily yield from funding will be: Funding Fee = Position Value x Funding Rate

Let’s use 0.087264% as it is on BTC right now, and assume that we hold 1 BTC on both the short and the long side.

Daily payment from funding: 1 BTC x $94,000 = $94,000 x 0,087264% = $82 per day ($29,930 per year)

Note that the funding payment at the end of the 1 hour interval on dYdX is:

position_size * oracle_price * funding_rate

Some thoughts about which assets to use for the strategy

If we use Laevitas, we can browse through all the assets that are supported on dYdX to see the current APR + the 1w (weekly average APR). Both are important parameters in making a decision on which asset to choose.

Let’s look at Fartcoin for example, a big retail favorite. We can see that the current 1 hour APR is quite attractive, however, the 1 week avg APR is low (in this particular case it is because Fartcoin is recently listed, so we don’t have enough statistics). More volatile coins will have more upside, but also more downside.

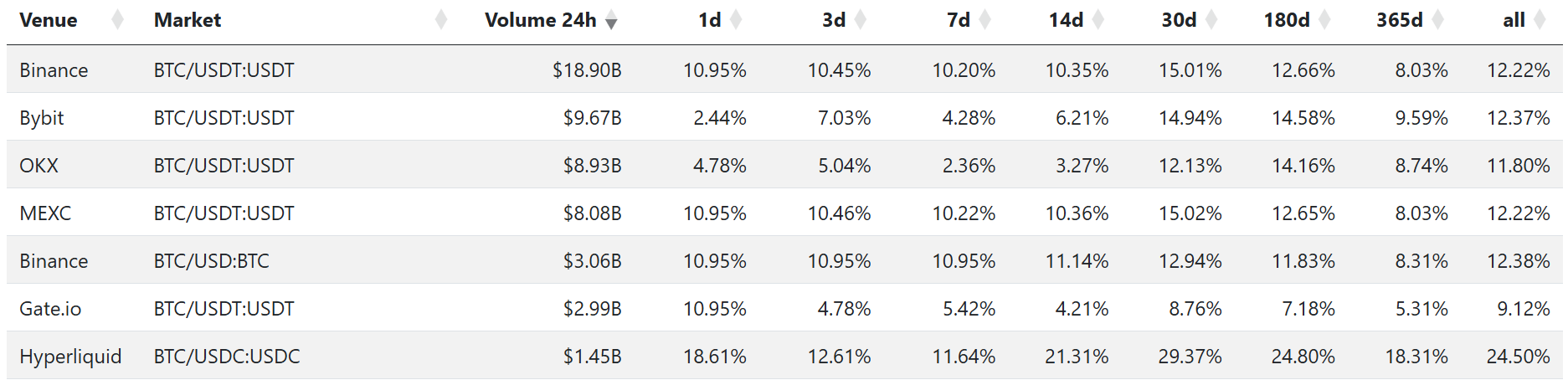

BTC on the other hand has 32% as the current funding APR and 20% as the weekly. To support it with more statistics, let’s look at BTC’s average funding through several exchanges (data from: https://basistrade.xyz/ ).

We can see that the average APR throughout the history of these exchanges hovers around 10-12% (Hyperliquid is the exception here, but it started in 2023 and has therefore a better looking data because it has been a part of a bear market).

This strategy definitely works better in a bull market, since more people are willing to leverage trade —> funding rate higher.

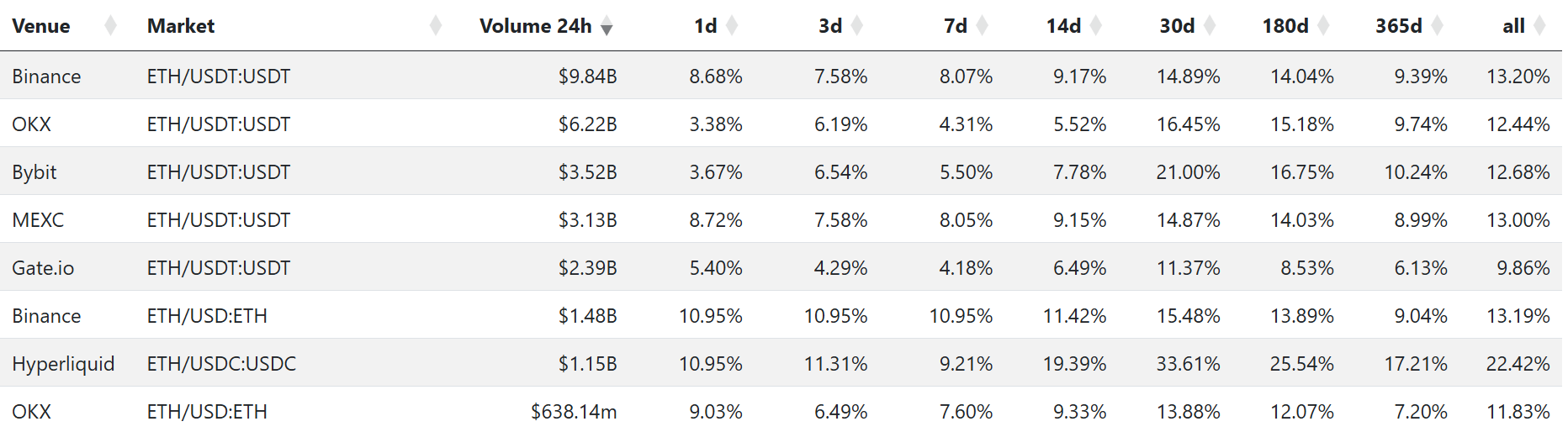

Just for fun, I pulled out the data for ETH as well, which is slightly higher (10-14% APR). On the long side you could also include a yieldbearing ETH variant which nets you 3,5% (stETH, weETH, mETH++).

Well, what is the perfect asset for this strategy? I’d say the answer depends on how closely you follow the space and much online you’d like to be. If you want to collect 15-20% passively without much hassle, go for BTC or ETH. If you however want to try to catch some more upside, you might look into newer coins. PENGU, FARTCOIN, HYPE etc. has recently had an average of 50-100% over some weeks.

This will most likely go down, but if you’re willing to rotate, this might be an option. Another factor you have to take into the picture is that you need enough liquidity for the size you operate with. If you do it with less than 5 fig ($10,000), this won’t be a problem most of the time, but again, always check the liquidity. With more newer coins, also comes more volatility, which means you have to rebalance more often and could be closer to liquidation risk + leg risk.

Let’s look at some of the risks/challenges.

Risks with doing a delta-neutral strategy

-opening long/short simultaneously is hard (leg risk): go and look at dYdX/Binance/Bybit on the prices for BTC on spot vs. BTC on perp/futures. do you see a difference?

As I am writing this right now the price is $93,840 on spot and $93,760 on perp.

First of all, how do you do it? Try yourself with a small amount and see that it will basically be impossible to catch the perfect long/short. The spread in this case is $80.

Should you go long first and then hope that the price increases so you can short higher? Or should you short first and hope that you can buy spot lower? Should you DCA and hope that you get an equal long/short entry?

-fees for open/close perp and open/close spot: this is obvious, but you have to pay trading fees for opening and closing positions, so if you don’t plan on holding for at least 24 hours you might lose due to trading fees

-rebalance if low capital: you’re equally long and short. what happens if you’re very skewed? like, let’s say BTC doubles and goes to $180,000. Your position would now be deeply red, while your long position is very green. Watch out for liquidation.

-liquidation risk: Depending on the amount of capital you have available on the exchange, you’ll be in danger of getting liquidated on the short side if the position goes very much against you.

-funding can (and will change): pretty self explaining…

-closing long/short simultaneously will be equally hard as opening: not much more to say about this, see the first point.

-CEX risk: what if Binance/Bybit goes under? Similar to smart contract exploit in the DeFi world

-fat finger: if you’re not experienced with perps you should be very careful. Over and over again you see people buy market orders that create giga wicks and you end up getting a very bad price (study liquidity, anon). Also, it’s just a push of a button to close/long a position. Be careful so that you don’t fuck up the trade.

…

That is it for today.

See you in the orderbook, anon.

Want To Sponsor This Newsletter? 🕴️

Send me a DM on Twitter: https://twitter.com/Route2FI or reply to this email. I have a sponsorship deck I can send you.

If you just want to follow my journey on Twitter, you can simply just follow as well :)

Join My Free Telegram Channel 🐸

I’ve launched a free Telegram channel where I share tweets, threads, articles, trades, blog posts, etc. that I find interesting within crypto.

Join it for free here: https://t.me/cryptogoodreads

Great post route2fi!

Really enjoyed reading and learning about this strategy.

I have two questions for you:

I am not very familiar with Hyperliquid, what’s the added value of that protocol?

To calculate the net APR someone would just need to substrack the trading fee + opening/closing trade position to the funding yield? Or I am missing something?